AVITA Medical Inc. AVHHL Dilution Risk Rises with New Perceptive Warrant Agreement

AVHHL

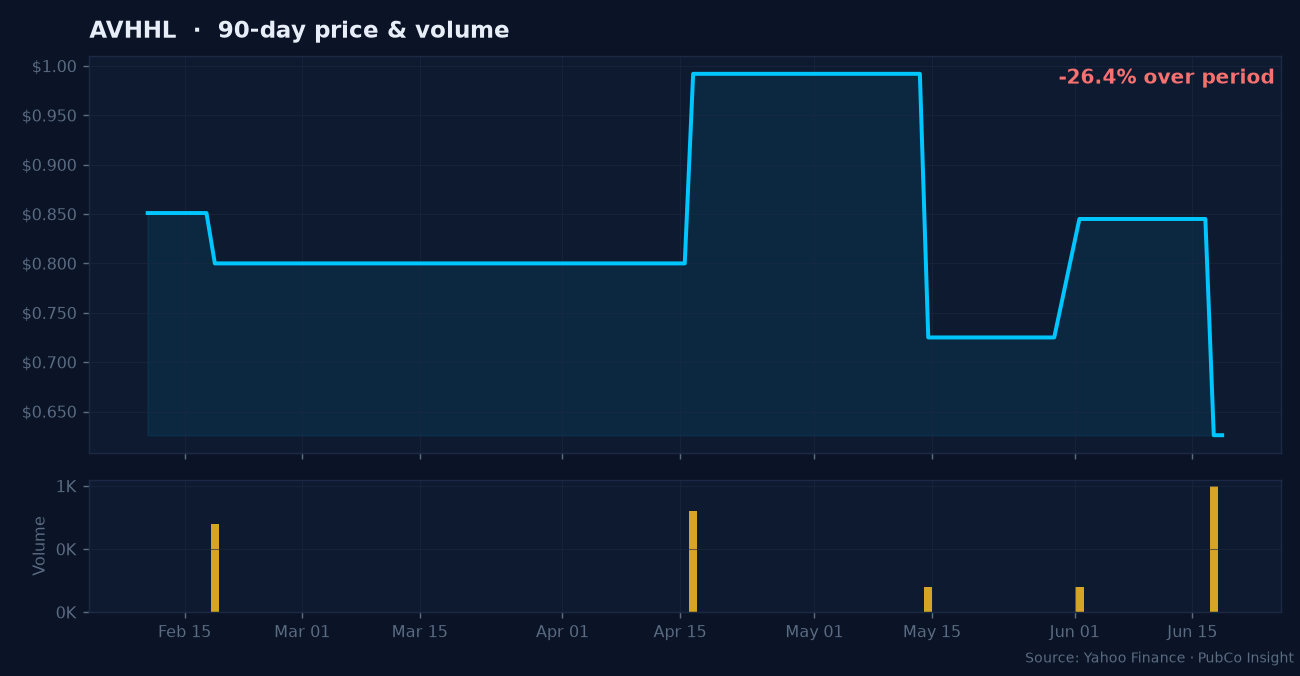

When a medical device company with a 123 million dollar market cap starts filing a flurry of Form 4s alongside a fresh prospectus supplement, retail investors should look past the clinical trial PR and focus on the capital structure. AVITA Medical, trading under the ticker AVHHL on the OTC market, recently triggered a series of regulatory filings that point to a shifting balance of power between existing shareholders and institutional creditors.

The critical development arrived on June 8, 2026, when the company filed an 8-K under Item 1.01, disclosing a new material agreement. Concurrently, AVITA filed a 424B5 prospectus supplement detailing a warrant transaction with Perceptive. This is the classic mechanism of microcap financing: securing capital today by pledging the equity of tomorrow. For retail investors holding the 30.78 million outstanding shares, this structured deal introduces a clear path toward dilution.

The data shows a high dilution risk score of 18, backed by a perfect storm of regulatory indicators including active S-filings, 424B prospectus supplements, and historical quarterly reports that require constant capital injections. While the company operates in the surgical and medical instruments sector where research and development costs are notoriously high, the reliance on structured warrant deals with institutional players like Perceptive highlights the high cost of keeping the lights on.

A subsequent wave of Form 4 filings between June 9 and June 12, 2026, shows active insider transaction reporting, a common occurrence when new financing terms are set or options are adjusted. When institutional lenders receive warrants, they gain the right to acquire shares at predetermined prices, which often caps the upward momentum of the common stock as those warrants are exercised and sold into the market.

Understanding the mechanics of a 424B5 filing is essential for anyone trading AVHHL. It is not an operational milestone or a commercial partnership, it is a financing tool. Investors need to weigh the company's clinical pipeline against the reality of a capital structure that is increasingly beholden to institutional warrant holders who have a very different risk profile than retail buyers.

Primary sources (SEC EDGAR)

4 2026-06-12: https://www.sec.gov/Archives/edgar/data/1762303/000119312526269544/xslF345X06/ownership.xml4 2026-06-10: https://www.sec.gov/Archives/edgar/data/1762303/000119312526266397/xslF345X06/ownership.xml4 2026-06-09: https://www.sec.gov/Archives/edgar/data/1762303/000119312526263968/xslF345X06/ownership.xml8-K 2026-06-08: https://www.sec.gov/Archives/edgar/data/1762303/000176230326000011/rcel-20260605.htm424B5 2026-06-08: https://www.sec.gov/Archives/edgar/data/1762303/000176230326000010/424b5_-_perceptive_warra.htm4 2026-06-05: https://www.sec.gov/Archives/edgar/data/1762303/000170998926000011/xslF345X06/ownership.xmlSee the dilution and promotion flags before you see the pitch.

Each week: the micro and small-caps now showing dilution or paid-promotion signals, with the SEC filing behind every flag. No recommendations, no price targets.